The Canadian

Quantum

Ecosystem

Report2024

Table of contents

- Foreword

- Key Research Findings

- Notes on Sources of Data

- Overview of the Global Quantum Ecosystem

- Companies & Workforce

- Patents and Competition for Knowledge

- arXiv: Innovation and Talent

- A Snapshot of Academic Talent in Canada

- Social Media Self-Representation

- Quantum Skills Requirements

- Conclusion

- Post-Script

- Data Analyst & Authors

- Footnotes

Want a copy of the 2024 Canadian Quantum Ecosystem Report in your inbox?

Foreword

The Quantum Algorithms Institute (QAI) in British Columbia, Canada, has a mandate to support the economic growth of the world class quantum computing cluster in British Columbia.

This report is QAI's second annual research report aiming to describe and quantify the ecosystem of researchers, businesses and supporting organizations that are working to build a new industry based on quantum technologies and to understand Canada's standing in this nascent but internationally competitive industry.

The quantum sector is developing rapidly with significant technological advances being announced, with continued public and private investments in research and companies and with the importance of quantum as a strategic, sovereign technology that all countries want to access becoming ever more explicit.

Quantum companies are still addressing scientific challenges, even as they have received significant private sector investments for commercialization and the sector is so new that basic demographic information is not yet available.

The most striking feature of the quantum landscape - in Canada and around the world - is the paucity of quantum talent, which threatens to slow progress to the multi-billion-dollar market opportunities that have been identified for this sector, even as technological advances are moving the advent of commercial quantum computing from a twenty-year scientific endeavour to a 5-year engineering challenge.

Many technology sectors are competing for talent, with Artificial Intelligence (AI) being the latest. The focus of this ecosystem report is to gain a better understanding of Canada's quantum sector; it does not explore opportunities at the intersection of quantum and AI.

The data gathered by QAI has been supplemented by information provided by the National Quantum Strategy Secretariat in Innovation, Science and Economic Development (ISED) Canada and by Quantum Industry Canada. QAI is grateful for the contributions made by both of these organizations as their data provides additional valuable insights into the quantum industry in Canada.

Once again, this report has been created as an interactive, online document. In the online version, the Figures are interactive and can be explored. A static PDF version of the report can also be downloaded.

Louise Turner

CEO, Quantum Algorithms Institute

Surrey, British Columbia

June 2024

Key Research Findings

- International Competition is Driving a Rapidly Changing Sector

Companies, investments, national strategies and sovereign technologies are all areas of focus as countries continue to fund growth. Despite financial tightening, private equity investments in quantum startups still reached $1.71 billion in 2023. The second largest private investment globally in 2023 - US$100 million - was made in Canadian start-up Photonic Inc.

Advances in science and engineering are being made in companies around the world, bringing the prospect of a scalable, fault tolerant quantum computer closer, moving from a 20-year science project to a 5-year engineering project. - Lack of Workforce Data: QAI is Working to Fill the Gap

Accurate data on Canada’s quantum labour market remains scarce due to the sector's infancy and the lack of national data collection benchmarks. Internationally, workforce data is similarly elusive, although available information suggests that the global talent pool for quantum is proportionately similar to or smaller than that in Canada. The Quantum Algorithms Institute is innovating to build an accurate picture of Canada's quantum ecosystem and its status in the world. - Small Quantum Workforce - in Canada and Around the World

QAI estimates that Canada's commercial and academic quantum talent pool stands at 4,000 people - just 0.01% of Canada's 40 million population. This is small, but not unlike the quantum workforce in other countries. Canada's long-term investment in quantum research and vibrant commercial ecosystem make Canada a global leader in quantum. - Canadian Companies

Canada's 47-plus domestic quantum companies are closely linked to Canadian universities and are mostly small Canadian controlled private companies (CCPC). Canadians own 14% of all quantum-technology-related patents filed in Canada. The flurry of patent filings in Canada since 2015 points to quantum technologies transitioning out of research labs and into companies and reflects the increasing pace of international competition to deliver scalable, fault tolerant quantum computing. - Canada Continues to Build on its Early Commercial Successes in Quantum

Canada is punching above its weight in all aspects of quantum. Analysis of social media reporting shows that Canada is home to 5% of the world's quantum talent pool, although Canada represents only 0.5% of the world's population. Canadian researchers ranked 10th most prolific in the world in 2023, authoring 1,000 of the 75,000 quantum computing research papers published on arXiv.

Canada has a vibrant quantum business sector with quantum computing and software companies such as D-Wave, Xanadu, Anyon, Photonic, 1QBit, Good Chemistry and Nord Quantique leading internationally on commercialization, scientific advances and development of market-ready quantum solutions. - Global Need to Address the Shortage of Talent in Quantum

The quantum computing market is projected to reach US$45 - $131 billion by 2040. However, the paucity of quantum talent - in Canada and around the world - threatens to slow progress towards this high-value market opportunity. With talent shortages in established high tech sectors and international competition for highly qualified personnel (HQP) in Artificial Intelligence and other deep tech fields, the nascent quantum sector will require innovation in education, training and workforce development to reach its full potential

Notes on Sources of Data

Developing an accurate overview of the Canadian quantum ecosystem is a challenging proposition.

In 2022 and 2023, when gathering data for the first Canadian Quantum Ecosystem Report, researchers at the Quantum Algorithms Institute (QAI) found that not only was it difficult to obtain relevant data, but also that datapoints commonly used to develop an understanding of industry sectors simply did not exist.

Statistics Canada (StatsCan) typically develops and uses the metrics which become standard measuring sticks to understand the nature of an economic or industry sector in Canada. StatsCan databases include jobs and job titles, which are tracked through the National Occupation Classification system (NOC), companies and industry which are tracked through the North American Industry Classification System (NAICS), and post-secondary education programs supporting the sector which are tracked through Classification of Instructional Programs system (CIP). Canada’s NOC database articulates 40,000 job titles and was last updated in 2021. The NAICS database is due to be updated in 2024 and the latest variations to the database were provided in 2022, based on 2021 information. The CIP database was last updated in 2016, but no changes were made to the classifications established in 2010. The term ‘quantum’ is not used in any of these databases, so it is not yet possible to use government data to track jobs, companies, the industry sector or educational programs for quantum skills and technologies. For a nascent sector such as the quantum industry, this presents some challenges. Indeed, it is the lack of workforce data that was QAI’s impetus to develop an annual quantum ecosystem report in 2022/23.

To develop The Canadian Quantum Ecosystem Report 2023, QAI researchers built a picture of the scale and activities of Canada’s quantum ecosystem using online, publicly available data from national and international patent offices, from the academic publication database arXiv and from information volunteered on social media platforms by people who self-describe as working in quantum jobs, companies, universities, colleges and research institutes.

Based on feedback on the 2023 report from the quantum community and internal review of the data sources used, QAI has revised some of its research methodology. The Canadian Quantum Ecosystem Report 2024 provides better accuracy and clearer findings and delivers more insights into the dynamic and growing quantum ecosystem in Canada, as well as the position of Canada’s quantum ecosystem in the world.

The Canadian Quantum Ecosystem Report 2024 was developed using data from these additional sources:

- A 2023 analysis of Statistics Canada demographic and financial data of Canadian quantum companies for 2017–2021 provided by the National Quantum Strategy Secretariat in Innovation, Science and Economic Development (ISED) Canada.

- The 2024 Canadian Quantum Industry Snapshot data gathered by Quantum Industry Canada (QIC), Canada’s national consortium of quantum technology and allied organizations in a survey of its members in January 2024. The survey yielded insights based on information from 33 of QIC’s then 41-strong corporate membership.

- A QAI online survey of 150 people working on quantum projects mostly in the post-secondary sector in British Columbia, Ontario and Quebec.

- A QAI-commissioned review of quantum job postings by professional development and education specialists South Arm Training to support identification of skills shortages in quantum companies.

In 2023, The Canadian Quantum Ecosystem Report used information from publicly available sources, industry data bases such as Crunchbase and Pitchbook, as well as public announcements to provide the bulk of the data. This year, with the opacity of the data landscape remaining the same as in 2023, QAI researchers have taken a similar approach, but increased the scope of data accessed - leveraging additional datapoints from external public and industry sources.

With this more nuanced dataset and using ISED’s recent internal study based on Statistics Canada data, as well as data found in the public domain, obtained through manual data collection, and data derived from QAI’s 2023 Industry Survey, The Canadian Quantum Ecosystem Report 2024 provides a more granular look at the rapidly changing quantum industry sector.

Note: All dollar numbers in this report are given in Canadian dollars unless otherwise stated, and all numbers are rounded.

Overview of the Global Quantum Ecosystem

The global quantum sector is developing in interesting ways that are quite different from the development and growth of other high tech and deep tech industries in the last 150 years.

Public Sector Investment in Sovereign Technology

Quantum technologies are already seen as significant sovereign assets, as indicated by the growing number of national quantum strategies that now exist and the amount of money being invested in the sector by national governments. McKinsey’s Quantum Technology Monitor, published in April 2024, lists 28 national quantum initiatives receiving more than US$42 billion of public money.

In April 2024, US-based quantum computing company PsiQuantum announced an investment of US$620 million from the governments of Australia and Queensland for PsiQuantum to build a quantum computer in Brisbane, Australia. Commentary from Australia’s press highlights that this investment will support Australia to “become a net exporter in the quantum industry and a substantial player in the global race for a quantum computer.”

Building Talent for Sustainable Growth

Quantum computing promises a rapidly growing industry sector with the potential to out-grow today's US $670 billion semiconductor market. McKinsey's most recent projections anticipate a market for quantum computing in 2040 will be between US $45 and $131 billion. However, there is a chronic global shortage of quantum expertise to support this growth.

Canada’s quantum workforce is a good illustration of this talent gap. With a generous estimate of the number of people in our quantum research and business communities, our quantum talent pool of 4,000 people is just 0.01% of Canada's total population of 40 million. Building a workforce that can grow rapidly enough to provide the skills and expertise to capitalize on the commercialization of quantum will require urgent and radical rethinking of ways to educate, train and grow the quantum workforce, particularly in the face of existing talent shortages for deep tech companies which are already being exacerbated by the demand for talent in the newly growing AI sector.

Today’s US $670 billion market for semiconductors, which developed and grew over around 80 years, employs 2.3 million people in 2024, is growing at a rate of 100,000 people per year and is challenged to find enough people to support its growth. It is difficult to see how a newly minted quantum industry will have enough skilled people to support a US $131 billion market (or even a US $45 billion market) over the next 16 years without significant changes in education, training and professional development programs for quantum in countries all around the world.

Rapid Commercialization

Quantum solutions are also being commercialized far more rapidly than other advanced technologies have been in the past. The technological and scientific advances that underpinned the growth of the telecom sector from 1984 onwards – encompassing, inter alia, the Internet, mobile phone and satellite services, handheld devices, social media and 5G – were developed over decades of oligopoly investment in large research labs. Similarly, the growth of the semiconductor industry happened over an 80-year period, giving time to build a skilled workforce alongside the development of silicon technologies.

Many companies developing quantum computers today are still resolving scientific challenges (such as noise, qubit fidelity, scalability and error correction) even as they have already attracted significant private and public investments. In December 2023, for example, QuEra Computing Inc. and its academic partners at Harvard, MIT, the University of Maryland and the US’s National Institute for Standards and Technology (NIST) announced a technological breakthrough, demonstrating a mechanism to run calculations on a 48-qubit computer using full error correction. This was a significant scientific win and step towards QuEra’s delivery of a fault tolerant quantum computer.

For any other technology, this kind of scientific proof point would be a prerequisite for any significant commercial investment, yet QuEra raised US$17 million in 2021, two years before this latest scientific breakthrough. In a more extreme example, PsiQuantum, raised US$ 450 million in July 2021 in addition to the $620 million recently announced investment by the Australian federal and regional governments and ‘hopes to build an error-corrected computer by 2029”. These are both examples of the unique development of the quantum sector and reflect the intense international competition for early successes with quantum technologies and, in particular, the drive to have sovereign access to a fully functional, fault tolerant quantum computer.

Private Sector Equity Investments

The quantum sector is a challenging industry to build and support. Private investments in quantum companies appears to have peaked at US$ 2.35 billion in 2022. The rise of inflation, and the collapse of both the FTX Cryptocurrency Exchange in November 2022 and Silicon Valley Bank in March 2023 contributed to financial tightening and spurred talk of a ‘quantum winter’ (the idea that investors stop investing in quantum companies). However, significant private equity funding for quantum companies has continued, with US$1.71 billion being invested in quantum companies in 2023. McKinsey notes that only five of the top ten equity investments in quantum start-ups were valued at more than US $50 million. Notably for Canada, the second largest investment of 2023 - US$100 million - was announced by Canadian start-up Photonic Inc as the company came out of stealth mode in November 2023.

Technical advances

All of today’s quantum computers are Noisy, Intermediate Scale Quantum (NISQ) devices. A commercially viable quantum computer must resolve technical challenges of qubit fidelity, error correction, fault tolerance and scalability.

Technological advances are happening all the time in research labs and quantum companies. One significant improvement was the December 2023 QuEra error correction advance for a 48-qubit quantum computer (referred to above). Another was the April 2024 announcement from Microsoft & Quantinuum of a technological improvement to deliver “reliable logical qubits that reduce circuit error rates by 800x”. These and other technological improvements represent step-changes in the technologies underpinning the delivery of scalable, fault tolerant quantum machines - driving towards the creation of commercially viable quantum computers and supporting the movement of resources from academia and into businesses.

Shifting Timelines

Increased public and private sector investment in quantum technologies, the drive to commercialize quantum solutions and step-changes in technical progress all combine to suggest that commercially viable quantum computing is no longer twenty years away. Rather, comments made by Ana Paul Assis, Chair and General Manager EMEA at IBM Madrid and Jack Hidary, CEO of Sandbox AQ at a World Economic Forum panel in January 2024 and information that PsiQuantum is working to build an error-corrected quantum computer in Brisbane, Australia by 2029, demonstrate that large business players are working to a timeline that suggests commercially viable quantum computing is closer to just five years away.

Overall Trends

Rapid technological and business changes, a chronic shortage of talent, and international competition to secure quantum solutions as sovereign technologies make it important for Canada to understand the quantum sector at local, national and international levels. A detailed understanding of the sector will help Canada retain our lead in the commercialization of quantum technologies and build on our international reputation in quantum research.

Companies & Workforce

Methodology & Caveats

It is a challenge to try to work out how many companies are working on quantum products, services and solutions in Canada and how many people are employed in the sector (in both academia and business) because there is no reliable single source of information on the sector. The quantum sector is changing and developing rapidly; work is still being done on the science and engineering of quantum computing, networking and communications, even as companies have been established to build hardware and software solutions for the nascent quantum market. For The Canadian Quantum Ecosystem Report 2024, QAI researchers have made some changes to improve the accuracy of the results reported and have sought out new sources of data to gain a better understanding of the global and Canadian quantum ecosystems.

ISED Data

The National Quantum Strategy Secretariat in Innovation, Science and Economic Development (ISED) Canada has provided Statistics Canada (StatsCan) with a list of Canadian quantum companies to enable some analysis of Canada's quantum sector. The StatsCan data has the advantage of providing detailed information about revenues, profits and salaries that QAI alone is unlikely to be able to obtain, shedding additional light on the sector. This information is not publicly available, but ISED has shared its internal analysis of the most recent aggregate data, from 2017 to 2021, and has given QAI permission to include these findings in this report. The last two years of this data coincided with the onset of the Covid-19 pandemic, introducing some additional ambiguity. The ISED information has been aggregated, so the QAI data analysis team have been careful to use it thoughtfully alongside the other data sources to avoid errors and to draw useful conclusions.

The list of companies ISED provided to StatsCan is made up of 75 Canadian quantum companies that ISED is aware of in computing, communications and sensors. It includes those making hardware components (chips, photonics, lasers, etc.), cryogenic equipment, software, software simulators, networking equipment, quantum sensing products or services, cryptographic solutions, and quantum computers. The list is also likely to include companies with 'quantum-adjacent' or 'quantum inspired' products or services particularly for software solutions. Data from StatsCan does not include multinational corporations who have quantum operations in Canada, such as IBM Canada or Honeywell, because StatsCan is unable to disaggregate their quantum statistics from their other domestic operations. Financial data from StatsCan is based on 68 companies and demographic data is based on 60 companies.

Quantum Industry Canada Data

Quantum Industry Canada (QIC) is Canada’s national consortium of quantum technology and allied organizations. As of May 2024, QIC has 60+ member organizations. QIC surveyed its then-41 members in January 2024 and has provided QAI with a summary of some of its findings, based on an 80% response rate from QIC members. This information has been aggregated, so QAI researchers have been careful to understand the QIC information and to use it appropriately to avoid errors and draw useful conclusions.

QAI Data

Companies

Due to difficulties finding reliable information about Canada’s quantum companies and workforce in 2022-23, QAI compiled its own list of quantum companies based on a sophisticated search of online information and has refined this dataset by an in-person review of companies’ websites. QAI has identified 47 domestic quantum companies that fall into three broad categories: quantum enabling hardware, or software, or quantum adjacent companies; post-quantum cryptography companies and companies using or building quantum hardware (including computers), software or tools.

Conflicting Surveys

QAI intended to survey companies and individuals across Canada in early 2024 but found that both ISED and QIC were conducting their own surveys at that time. Three surveys asking for very similar information seemed counterproductive and QAI will explore opportunities to work with ISED and QIC to coordinate surveys and share data and results with ISED and QIC for future reports.

Snapshot of Academics

In early 2024 QAI conducted an online survey of 150 academics at post-secondary institutions in BC, Ontario and Quebec.

Quantum Startups

QAI’s data does not specifically identify quantum startups. QAI is engaging with business incubators and accelerators in Canada to learn more about new companies that may not have any web presence and intends to provide an overview of these companies and the quantum incubator/accelerator in future QAI reports.

Data & Analysis

ISED Data

Sector Growth, 2017 – 2021.

The number of quantum companies in Canada grew from 43 in 2017 to 65 in 2021. 60% of these 65 companies were making $750,000 or less in revenues in 2021. Over the same four-year period, revenues for Canada’s quantum companies increased from $103 million to $173 million and the number of people employed in the sector grew from 888 in 2017 to 1,389 in 2020.

The number of women in the commercial quantum workforce grew from 186 in 2017 to 306 in 2020, however the proportion of women in the workforce barely changed, moving from 20.9% in 2017 to 22.0% in 2021. Women’s salaries were between 29.6% and 35.5% lower than men’s salaries during this period – a significant disparity which cannot be satisfactorily explained without more granular information about the roles held by women and men in Canada’s quantum companies.

From 2017 to 2020, average salaries in the quantum sector grew from $61,662 to $66,872 per year. In 2021, the average annual salary for employees in the Information Communications & Technology (ICT) sector in Canada was $89,630, which is 52.5% higher than the Canadian average. (The Canadian average salary in 2021 was $58,774.)

QAI analysis suggests that, as quantum is a deep tech sector and a significant proportion of people working in quantum are highly qualified – many with PhDs – one might expect salaries in the quantum sector in 2020 to be higher – more in line with ICT salaries. The lower quantum salaries are likely to reflect the very early stage of commercialization in the quantum sector. Many companies in the sector are likely to be start-ups working on very low cash budgets, with employees earning low salaries but holding stock options in their companies. It may also reflect the extent to which many academics in quantum fields in Canadian post-secondary institutions have started quantum businesses and are not drawing high salaries because their main income source is their university salary.

Finally, a subset of the ISED data allows an examination of the age of employees in the quantum sector from 2017 to 2020. The overall number of employees grew from 900 in 2017 to 1,406 in 2020 – a 56% increase. Across five different age groups, (15-24, 25-34, 35-44, 45-54 and 55+) most employees each year were in the 25-34 age group, representing 32% of the workforce in 2017, growing to 38% of the workforce in 2020. The next largest age group was 35-44-year-olds (26% of the workforce in 2017, declining to 23% in 2020). While participation from all age groups grew over the four years, the number of employees in the 25-34-year-old age group grew aggressively- by a total of 48%. This age distribution shows that millennials (born between 1981 and 1996: aged 24 to 39 in 2020) are significant contributors to the quantum workforce.

Quantum Industry Canada Data

The 2024 Canadian Quantum Industry Snapshot was provided by Quantum Industry Canada (QIC), Canada’s national consortium of quantum technology and allied organizations. It reported on data collected from QIC’s member companies in January 2024.

Quantum Industry Canada’s survey paints a picture of Canada’s quantum sector being dominated by Canadian owned companies (82% Canadian Controlled Private Corporations), that are generally small (33% with 1-10 employees and 46% with 11-50 employees) with flagship products that are in the research phase (33%), the prototyping phase (46%), or the commercialization phase (12%). QIC member companies are headquartered across Canada, with 49% being based in Ontario, 24% in Quebec, 12% in British Columbia and 9% in Alberta.

QAI Data

Workforce growth and change

Last year, QAI researchers built a list of 44 quantum companies in Canada, employing an estimated 1,000 people. 2023 saw an approximate 30% increase in number of active participants in the Canadian quantum industry, based on 47 companies employing 1,300 employees this year. The quantum research brain drain that was identified last year remains: more researchers were leaving than coming to Canada, with the U.S. being the most common destination for outgoing quantum experts.

To measure the direction of demand for employees, QAI tracked the number of job postings on websites and found a 4% increase on average month to month, indicating the demand for workers in this field is on the rise.

Company Changes

While employment numbers are rising, QAI researchers found that between 2023 and 2024, one Canadian company closed its doors and another was acquired by a US-based company, resulting in a 3% attrition rate for companies across the sector.

Although the median age of Canadian companies is increasing, new companies are still being created, or emerging from start-up stealth mode. Last year, QAI identified 3 new companies within the Canadian quantum ecosystem, bringing the number of tracked companies to 47. It should be noted that this number excludes larger corporate entities with various business units (such as IBM, Microsoft, Google, and others) that have established workspaces or labs within Canada, because it is difficult to disentangle quantum-related business activities from other business activities.

Canada's Quantum Workforce: Comparing ISED and QAI Data

To assess the number of quantum companies and industry employees in Canada's quantum sector, both ISED/StatsCanada and QAI have excluded companies that have multiple lines of business where it is not possible to identify a specific quantum talent pool (for example, IBM or Amazon Web Services). To date it has not proven possible for ISED and QAI to compare notes on the companies each has counted as quantum companies.

The data available so far provides the following industry numbers:

| Data Source & Year | Number of Companies | Number of Employees |

|---|---|---|

| ISED/StatsCan | ||

| 2017 | 43 | 888 |

| 2021 | 65 | 1,389 |

| QAI | ||

| 2022 | 44 | 1,000 |

| 2023 | 47 | 1,300 |

Figure 1. Quantum companies and employees in Canada

QAI's list of quantum companies is smaller than that held by ISED. Both sets of numbers undercount the size of the commercial quantum workforce, leaving out employees in multinationals and larger companies with multiple business lines.

QAI researchers estimate that there are approximately 1,700 people in Canada’s commercial quantum workforce plus at least 166 quantum researchers in Canada's post-secondary sector plus researchers in private research institutes and Master’s and Bachelor’s degree candidates giving an estimated quantum talent base of no more than 4,000 people in Canada.

Canadian Companies in the News

Anecdotally, there are also plenty of publicly reported events that show activity, technical progress and investment in Canada’s quantum computing sector.

- In January 2023

Toronto, ON-based quantum computing company Xanadu received a $40 million grant from the Federal government. - In June 2023

Burnaby, BC-based quantum computing company D-Wave, which had floated as a public company on the New York Stock Exchange (NYSE), moved its headquarters to the United States. - In November 2023

Coquitlam BC-based quantum computing company, Photonic Inc, came out of stealth mode, announcing a US$100 million investment from BCI (BC’s pension investment firm), Microsoft and others. This funding round was recognized as the second largest venture capital/private equity investment in the world in quantum technology startups in 2023 by McKinsey.

Canada's commercial quantum ecosystem is growing and adapting to international competition. The data required to describe and fully understand the sector is not yet available but QAI and other players in the Canadian quantum ecosystem are working to fill this gap.

Patents and Competition for Knowledge

Methodology & Caveats

The data on patents presented in The Canadian Quantum Ecosystem Report 2023 was drawn from patent descriptions clustered using the Bidirectional Encoder Representations from Transformers (BERT) language model to provide a window into how types of patent clusters formed around quantum subjects. The BERT analysis was applied to patents from every accessible patent office worldwide, but the 2023 analysis focused on data from the major quantum industry hubs: China, US, Europe, Japan, South Korea, Australia, Canada, Taiwan, Denmark, Russia, UK, Brazil, Spain, France, and Netherlands, along with an overview of worldwide patents. This data was used to identify common subjects for quantum patents and trends in the volume of patent applications being filed and granted over a 50-year period.

For this 2024 report, QAI researchers focused on Canadian patent information. Recognizing that patents may be filed in multiple agencies at any given time, “Canadian” patents were identified based on applications submitted by organizations based geographically in Canada and patent applications submitted to the Canadian Patent Office.

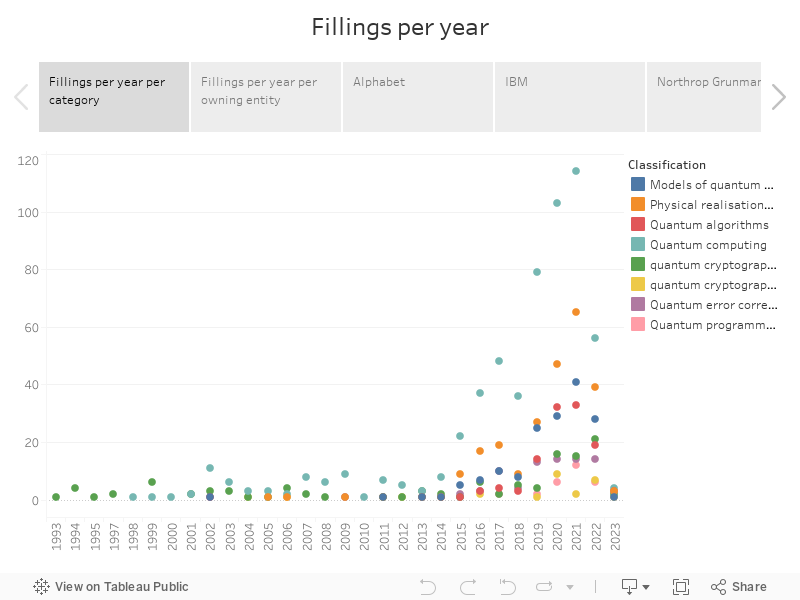

The patent dataset for this report used patents classified under specific IPC (Identification, Preservation and Collection) codes (see the chart below for exact codes). A total of 1,329 quantum patent applications were submitted in 2023. Of these, 1,308 fell into the categories used for QAI researcher analysis.

| IPC Category | Category Code | # of Patents |

|---|---|---|

| Quantum computing | G06N10/00 | 578 |

| Models of quantum computing | G06N10/20 | 160 |

| Physical realisations or architectures of quantum processors or components for manipulating qubits | G06N10/40 | 241 |

| Quantum algorithms | G06N10/60 | 114 |

| Quantum error correction, detection, or prevention | G06N10/70 | 76 |

| Quantum programming | G06N10/80 | 29 |

| Quantum cryptography and communication | H04L9/0852 | 110 |

Figure 2. Quantum Patent Identification, Preservation and Collection (IPC) Code. Number of Patents Filed in Each Category.

Working with a smaller, more closely defined dataset allows for a more detailed examination of available data. For example, with fewer patent applications, it was possible to identify the headquarters of all entities filing Canadian patents, allowing patent applications to be assigned their “parent” country.

Patent trends identified in this report are based on filing priority dates (the dates on which the patents were filed) for patents filed in Canada and focuses on Assignees (the entities that will benefit from the patents) rather than patent Authors (the person or group responsible for developing the innovation).

Although tracking the number of patents does provide a window into innovation, it also poses some challenges for data interpretation because applicants may apply for patents in many countries, and the patent granting process takes time: up to 4 years in Canada, with similar wait times elsewhere.

Figure 3. Number of Patents Filed in the Canadian Patent Office by Year and IPC Code

Data & Analysis

Patents

Figure 3. shows patents filed in each of the IPC categories of interest in QAI's research. Of the 1,308 patents referred to in the table, only 110 related to cryptography and communication with the bulk of the patent applications relating directly to quantum computing or to the hardware or software integral to successful quantum computation.

While most historical quantum-related patent filings are related to academic or public institutions, the surge in filings since 2015 has mostly been associated with the corporate world, indicating that breakthroughs are moving from the domain of research into the domain of industry. D-Wave Systems led this shift with the 2009 patent wave that foregrounded the release of their computer, followed by Northrop Grumman and ID Quantique from 2009 to 2012. These waves are indicators of companies seeking to cement their foothold in the field as this new market grows.

Drilling into specific classifications and using the most prolific patent owners as examples, two trends in patent applications can be observed. First, multinational companies like Google and IBM have very diverse applications touching every quantum patent category. However, all of their many patent applications were made in the period from 2015 to 2022. Second, historical players like Northrop Grumman and D-Wave Systems have been applying for high level G06N10/00 patents since 2008 but have diversified since 2015, adding patents related to more specific applications (/40, /60 and /70 being the most prevalent).

The current corporate frontrunners are Google, IBM, Northrop Grumman, and Zapata, representing together about 40% of patent filings between 2019 and 2022. If these top applicants are removed, the curve of patent applications for all other entities reaches a peak in 2019, with all other years seeing overall growth but no flurry of activity. This represents linear growth with each year being only a bit more than the last, except 2019 in which data shows as a spike in quantum computing applications that does not follow the trend. Fewer or less pronounced waves may point toward industry maturation in some sectors.

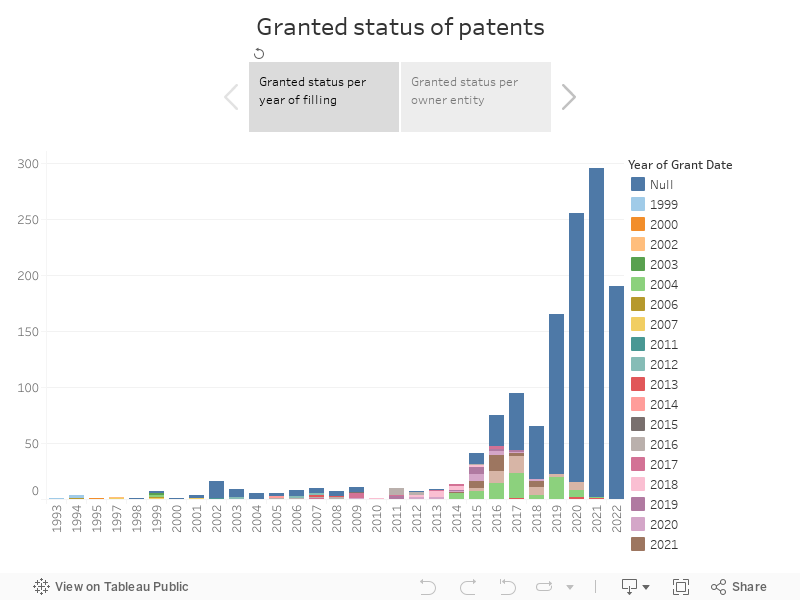

Figure 4. Canadian Quantum Patents Granted by Year

Figure 5. Canadian Quantum Patents Applied for and Granted by Year and by Organization

Patents and Industry

The data provides some noteworthy outliers and segments in patents. Northrop Grumman, for example, is not only the only defense contractor in this space, it has also seen most of its patents granted with only the most recent still pending, and IBM’s patents have been filed in less time than it takes on average for patents to be granted. As IBM has patents still waiting to be granted, it is hard to judge the effectiveness of their strategy.

Likewise, Google is noteworthy not only for its volume but its trajectory; representing about one fifth of all patents since they first filed in 2014. Google has also had an above average rate of patent success, with its patents being granted faster than most others. When compared to other entities with more than 10 total patents, only 1-Qbit and D-Wave Systems are competitive.

Patents and Academia

QAI researchers divided the dataset between patent applications from companies versus those from universities. Canadian university IP rules vary from institution to institution, but overall, QAI found very few patents filed by individual researchers themselves.

The Canadian patent office appears to be considerably slower to grant academic patents than business patents, independent of year of application. While the time between filing and granting is long for both academic and commercial patents, the difference lies in the volume of successful applications coming out in the last few years. If normalized for volume, on average, academic patents are 23% less likely to have been granted than corporate patents. This distinction is of interest, but the cause is unclear. What the data shows, however, is that the common wisdom that academic patents are more “fundamental” than corporate patents, and should therefore be easier to obtain, does not appear to hold true.

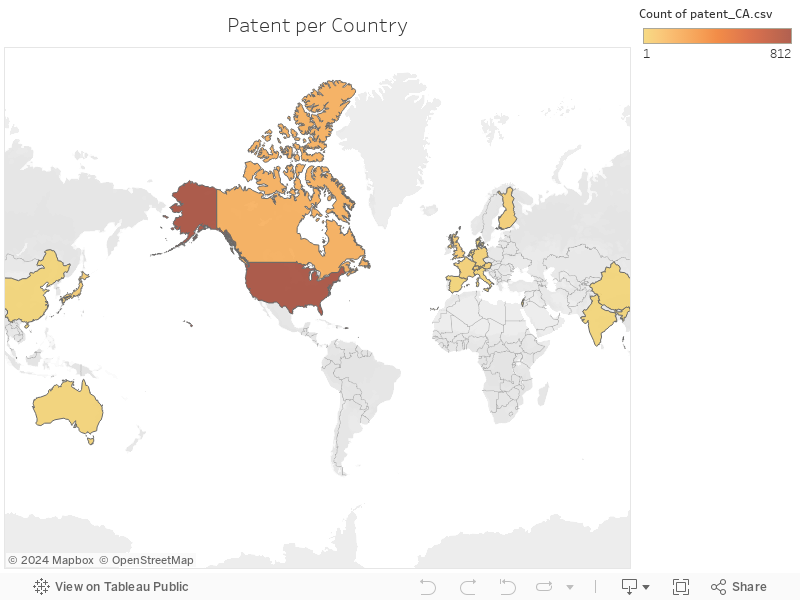

Figure 6. Location of Owners of Canada's Quantum Patents

Location of Owners of Canada’s Quantum Patents

Data gathered about the geographic location of patent owner's headquarters is shown in Figure 6. These patent numbers follow a pattern similar to Canada's commercial links to other countries. Indeed, Canada’s main trading partner, the United States, represents 61% of all granted quantum technology related patents. The second region, Europe, represents 17% of patents, with the UK being just over 4 points of that number. While China and India fall below 1% each, Japan stands at 3% which places them third overall.

Overall, Canadian owners represent 14% of all quantum-technology-related patents filed in Canada - a strong indicator of the internationally competitive nature of the quantum sector. Until 2014, Canadian owners represented more than half of all quantum patent applications filed in Canada. After 2014 American corporations began filing applications en masse, reflecting a transition of the quantum market to a more commercial focus in 2014-15. Industry and corporate patents indicate major players are staking out business niches. Data collected may indicate the quantum technology sector is reaching a more mature stage, but that can only truly be known in hindsight.

Methodology & Caveats

Publications: arXiv

The Canadian Quantum Ecosystem Report 2023 relied on data about publications gathered from arXiv in the quant-ph, cond-math, quant-gas, math.qa, and gr-qc categories. The current report does the same, with the addition of papers from cs.ET. This new set has helped to minimize the error rate of papers not related to quantum computing. Using this smaller but more exact dataset, QAI researchers developed a more precise understanding of the quantum computing research world.

The set of 1,430 papers analysed for the 2024 report represents the work of 4,229 authors worldwide, which, while being more precise than in the 2023 report, is significantly smaller and brings with it some challenges. Most notably, with the smaller dataset, no inference can be drawn about where a paper's author or authors live. This is in part because, by a quirk of the quantum computing publishing world: authors typically put multiple affiliations on each paper, including affiliations to multiple countries.

Use of arXiv is not uniform worldwide, or even within the Canadian quantum technology ecosystem. For example, the Netherlands hardly appeared in the arXiv search results, while certain American institutions had exceptionally high numbers. To estimate the discrepancy between the arXiv publication numbers and actual numbers, QAI researchers went to the personal profiles of individuals from 5 different institutions from around the world (USherbrooke, MIT, TUDelft, ETH Zurich, and IIT Hyderabad) and manually compiled precise numbers of quantum publications from each of these institutions. From those numbers, the difference between the arXiv number and the actual number was calculated, and the ratio from that difference was used on the rest of the dataset, giving researchers, and the reader, a sense of the margin of error.

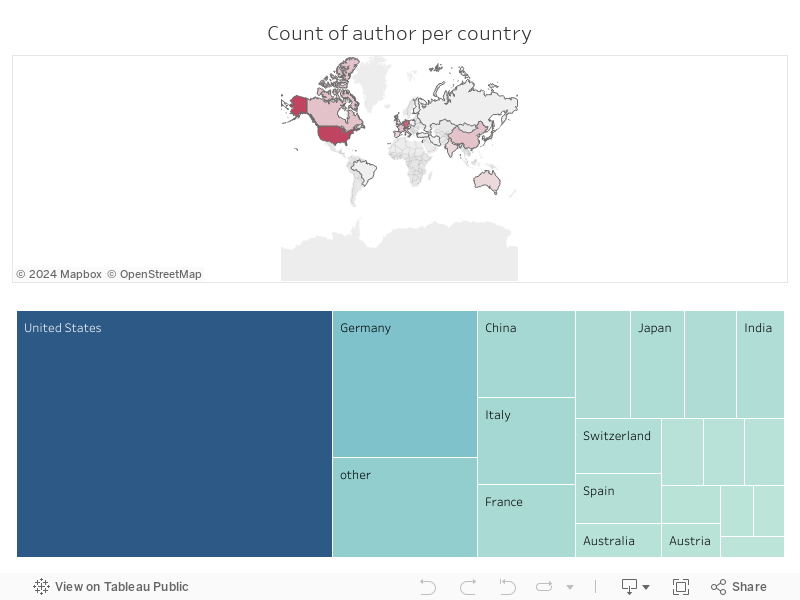

Figure 7. Count Academic Papers on Quantum Computing by Country

Figure 8. Count of Authors by Country.

Data & Analysis

Publications: arXiv

Worldwide, about 75,000 academic papers on quantum computing were published in 2023, a rise since 2022 when there were 73,500 papers published. While there has been some movement in the ranking of the countries with the most publications (notably, the Netherlands, which was 51st in terms of publication volume in 2022, is now 15th), the top publishing countries remain remarkably similar to 2022, with the United States in the top spot (with more than 12,000 papers in 2022) and China (with more than 7,000). This is a remarkable datapoint as United States currently represents 41% of researchers around the world, while China appears to represent only 5%. Because China is culturally and politically so unlike the other countries surveyed, reliable conclusions about the state of quantum research in China cannot be drawn from this comparison.

European countries also provide a challenge for analysis. When grouped as a block, western European countries have a leadership position with about 14,000 shared publications and about 32% of the world’s researchers, but when separated the picture shifts: Germany leads within Europe with a little under 4,000 publications and 11% of the world’s researchers. Italy, the United Kingdom, France, Spain, and Switzerland all follow with between 1,700 and 1,000 publications and each host about 4% of the researchers. India and Japan stand at around 2,000 to 2,500 publications, while Canada and Australia hover around 1,000 papers each, and Canada, India, and Japan each have about 3% of the world’s researchers.

International Collaborations

Collaboration is a hallmark of the quantum sector. The numbers paint a portrait of a quantum computing research world which resembles the quantum computing business world in terms of volume (both in terms of investment and patent activity) and indicates a positive correlation between talent and business growth.

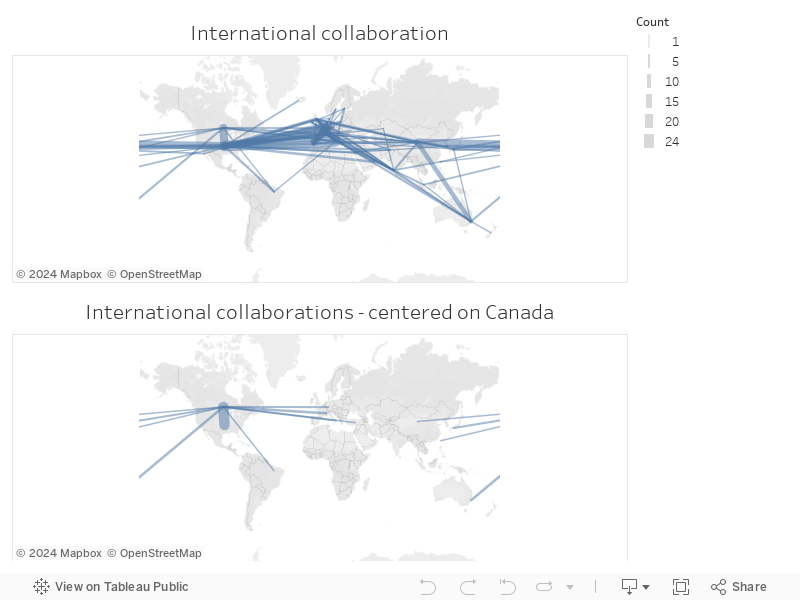

Despite the importance of collaboration, estimating research collaboration per country is difficult. QAI researchers used a methodology similar to that used to estimate researcher output, and this resulted in a small dataset. A consequence of the relatively small size of the dataset and of the unequal usage of arXiv between countries is that the data must be treated with skepticism. The smaller dataset shows, for example, a dearth of collaborations for certain countries such as Italy, Canada, Australia, and Switzerland. Based on QAI’s 2023 data and on anecdotal evidence, Italy, Canada, Australia and Switzerland all have large communities of quantum researchers who are active in international collaborations. QAI researchers applied a similar correction estimation to the collaboration subset as to the overall data set. This indicates that about 24,000 international collaborations can be estimated, with 12,000 from Europe, 3,000 from the United States and 1,000 from Canada.

Figure 9. International Collaborations on Quantum Academic Papers, 2023

Figure 10. Canadian Collaborations on Quantum Academic Papers, 2023

Collaborative and mutually beneficial relationships between academia and the business world appear to be an important contributor to high outputs. In 2023, 32% of the total output of the 1,430 papers published (459 total) in the quantum computing research landscape involved some form of international collaboration. Europe emerged as a central hub for international collaborations, participating in over half (51%) of these alliances; 73% of the European collaborations are within Europe. This is indicative of a strong intra-continental network and of the positive impacts of intra-European accords. Notably, Italy, the United Kingdom and France each account for 6%, and Spain for 5% of the collaborations overall.

The United States also plays a significant, though much smaller role, contributing to 12% of the international collaborations, reflecting its ongoing investment and interest in quantum technologies, while India represents 6% and Japan stands at about 4%.

Canadian collaborations on academic papers on quantum are shown in Figure 8. Canada contributed to 4% of the overall collaborations in 2023. Of those, 52% involve collaborators from the United States, underscoring the strong research ties between both countries. 20% were collaborations with Europe: that number is expected to grow with Canada’s recent association with Horizon Europe, the EU’s flagship research and innovation funding program. Among Canada’s EU collaborators, France (8%), Italy (5%), and Germany (5%) have been the primary partners. Additionally, Australia emerges as another notable collaborator, involved in 8% of the partnerships with Canada.

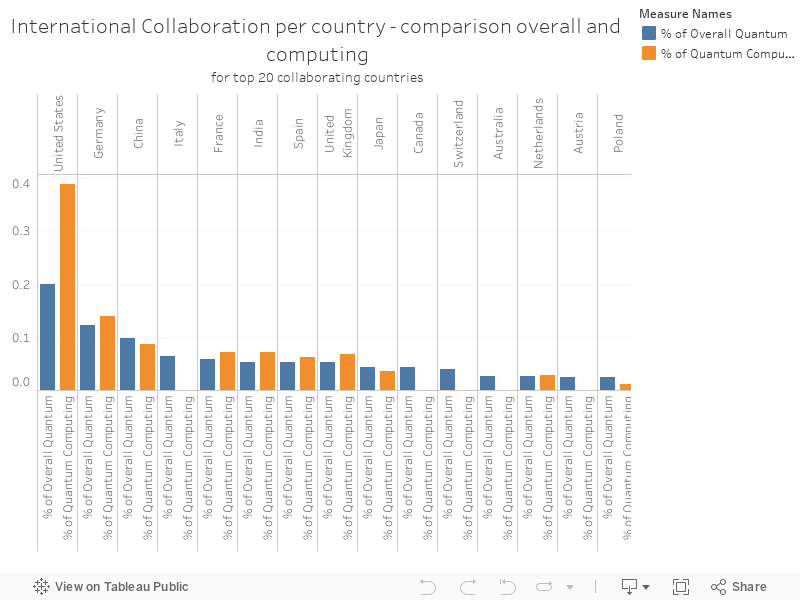

Figure 11. Top 20 Countries with International Collaborations on Quantum Papers, 2023 - All Quantum Papers and Quantum Computing Papers

Canadian Researchers and Authors

For Canada, the smaller, more accurate selection of arXiv papers used for this 2024 Ecosystem Report has helped to capture some cultural nuances within different academic institutions and provided QAI researchers with a more detailed look at different components of the ecosystem. Readers of the 2023 report queried the absence of papers from the University of Sherbrooke in the 2023 analysis of arXiv papers. Data for the 2024 Ecosystem Report indicates that researchers from the University of Sherbrooke rarely publish papers on arXiv, while those from the Perimeter Institute use it more than average.

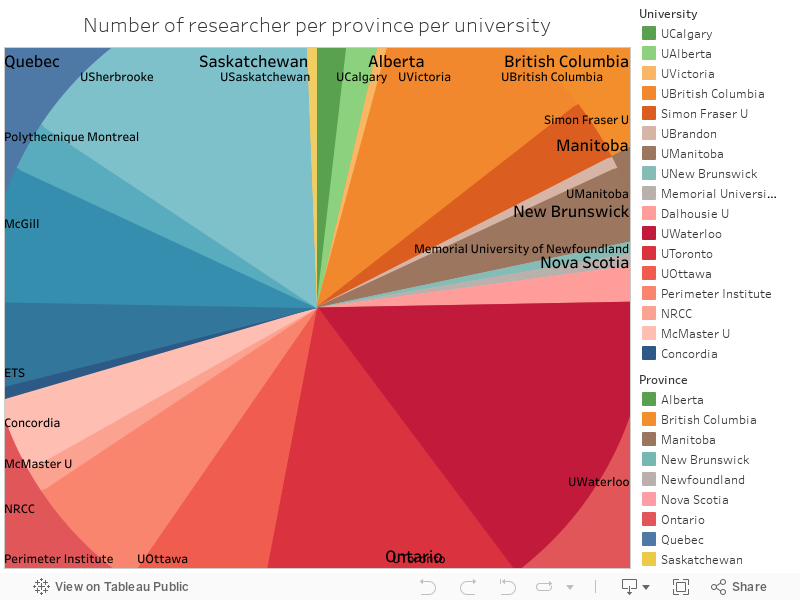

Figure 12. Academic hot spots

Innovation occurs across Canada, but data also shows distinct academic hot spots. Historic trends continue this year with Ontario, Quebec, and British Columbia representing most research done in the quantum technology fields. Universities with the most researchers in the quantum fields are University of Waterloo, University of Toronto, University of Sherbrooke, and University of British Columbia, with some notable outliers, including the University of Ottawa, ETS, and McGill, each of which have authors with more than fifty publications in the last year.

Size and relative impact of each province, based on citations and h-index, is proportionate to the size of the province's business ecosystem, showing a strong correlation between business investment and academic research. This trend also can also be observed at a national level, comparing countries where the size of quantum ecosystems correlates strongly with GDP and economic development.

A Snapshot of Academic Talent in Canada

Methodology & Caveats

Among the key findings of The Canadian Quantum Ecosystem Report 2023 were indications of how talent flowed from one country to another and how academics moved during their careers. Among the most critical findings was that individuals were leaving Canada faster than Canada was attracting them. Gathering this data was difficult, and conclusions based on this data must be made with a thorough understanding of the data's limitations.

To understand more about the workforce in the quantum business sector, QAI researchers gathered data from social media in both 2023 and 2024. This methodology was chosen to compensate for the lack of official data and the lack of standard job titles or job descriptions. The data was collected based on information volunteered on social media platforms, with people providing their own job title and description, which means the exact number collected must be understood as being imprecise. This lack of precision compels QAI researchers to only share aggregate data per country and comparative data year to year, based on the idea that cultural shifts in the ways people self-represent their job titles should be comparable year to year (while not necessarily being true for a longer period). Future research on parameters of job titles and job description will be necessary to ensure this methodology captures any cultural drift. It is also important to note that social media usage is not perfectly comparable country to country.

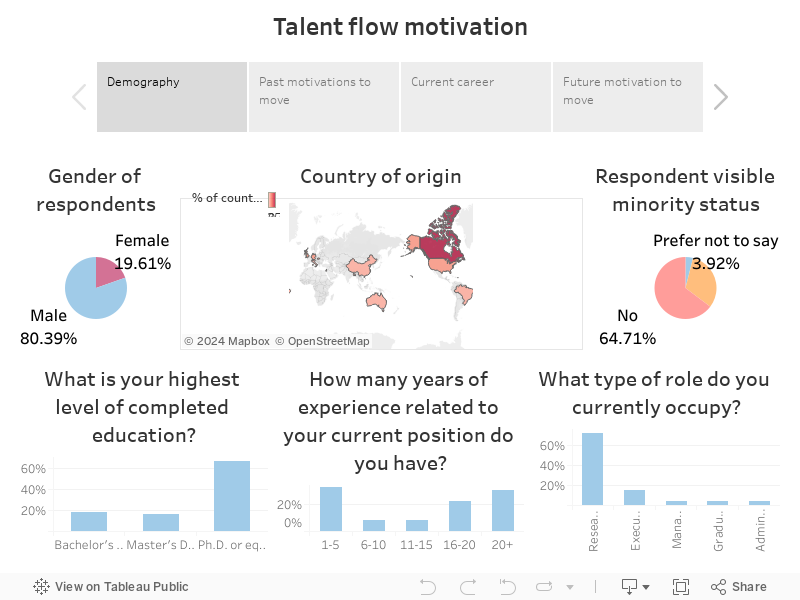

To better understand earlier data on the location and motivations of Canadian quantum researchers, QAI launched its Quantum Research Workforce Survey in 2023. This survey was designed to learn more about the underlying factors that motivated highly talented individuals in Canada’s research community to move. Researchers gathered the responses of 53 quantum experts from British Columbia, Ontario, and Quebec - about 1/3 of those who received the survey. Of the respondents, all but 2 were academics working in Canadian universities, providing a snapshot of Canada’s academic landscape in the quantum sciences. The survey was structured in three sections: Demographics (to provide data about the talent pool and its challenges), migration and motivation, and current career and motivations.

For future surveys, quantum industry and business experts will be targeted more thoroughly, as their career trajectories should be different, and their data will provide an important window into the talent landscape of both Canada’s academic and business sectors for quantum.

Data & Analysis

Demography and overall results

Figure 13. Gender of Respondents, Country of Origin, Visible Minority Status, Level of Education Career Experience & Professional Role.

A detailed breakdown of information gathered by QAI in the Quantum Researcher Survey can be explored in the online version of this report.

Among 51 respondents, 80% identified as male and 20% as female (0% as non-binary or other). This is in line with the ISED/Stats Canada findings for Canada’s workforce from 2017 to 2021, reported earlier. 31% self-identified as a visible minority and none identified as having a disability. 36% of respondents listed Canada as their country of origin, while another 35% came from European countries. 9% were from the United States while 4% identified their home country as China, 4% Australia, 4% Brazil, and 4% Israel.

Of all respondents, 72% were researchers working in academic institutions, and only 20% had varying positions in private companies. Two thirds had PhDs, and all others were either Bachelor's or Master's degree alumni in equal amounts.

76% of respondents reported having moved from one country to another for their careers. Of those moving country, career advancement was almost universally a motivating factor, with 84% of respondents scoring it a 4 or 5 out of 5. Skill development, identified by 65% of respondents, was the second most common reason for moving countries. Networking/industry opportunities, change of environment, and personal growth each motivated around 50% of respondents.

When asked how satisfied they were with their careers, 88% of respondents gave a satisfaction level of 7 or more out of 10. Seventy per cent felt they would need more training or education to get their career where they would like it to be.

Asked if they would move countries in the future for career reasons, about 25% of respondents gave a score of more than 5 out of 10. Likely reasons for such a move are less polarized: with career advancement and higher compensation being slightly higher motivations than work life balance and family considerations.

Career satisfaction

When looking at the level of job satisfaction declared by respondents, the first thing to note is that all but 2 respondents rated their job satisfaction 5 out of 10 or higher, with more than two thirds saying 8 or more. Even allowing for the possibility that respondents may exaggerate their level of satisfaction, encouraging trends can be extracted from the data.

When career satisfaction is looked at from a diversity and gender angle, the differences in averages for both fall to within 5%. This follows trends observed in the overall job market but outperforms other high-tech sectors in which the gap hovers around 8-10%.

The most significant determinant of career satisfaction seems to be experience in related roles with respondents in the 0–9-year group rating job satisfaction at an average of 6.75 out of 10, the 10-19 years group at 7.54 and the 20+ year group at 8.53. This gain of a point of satisfaction per 10 years of experience could be explained by factors such as getting access to better job opportunities or securing more stable or better paying jobs, but it could also reflect different expectations and values held by younger and older generations.

The second most significant factor influencing career satisfaction was the choice to move from one country to another for career advancement. Those who had moved in the past showed a full point more satisfaction than those who had not moved, with those that moved reporting an average of 8.15 and those who did not reporting 7.2 for satisfaction. Here a potential positive loop is noticed in which respondents, having prioritized their careers enough to make a move, might see their careers in a more positive light than those who did not, irrespective of actual condition. However, studies on the impact of mobility point towards moving having positive impacts on careers.

Analysis of survey data revealed that among various motivations for job relocation, only family consideration positively impacted future job satisfaction, increasing it by 5%. In contrast, other motivators such as change of environment, work-life balance, and personal growth showed around a -10% satisfaction rate, while prestige/recognition had the worst impact at -20%. Interestingly, early-career respondents were twice as likely to be motivated by prestige/recognition, whereas those moving later in their careers were almost twice as likely to be motivated by career advancement, which resulted in less than a 1% change in career satisfaction.

Overall, it seems that those who move later in their careers end up more satisfied than those moving in the first 5 years but not by an amount that should push people one way or the other; 5,1%. In parallel, if the result is taken as an indication of the motivators that have a positive correlation with career satisfaction, the clear winner is personal growth, and the clear loser is prestige/recognition. Respondents who were highly motivated by personal growth declared a career satisfaction score 13% higher than the average, while those motivated by prestige/recognition ended with a score 8% lower than average.

Perspective on the impact of diversity

When respondents are broken down based on gender and visible minority status to create two groups, 1) white male and 2) diversity/women, and respondents who preferred not to say about either gender or visible minority are removed, white males represent 52% of respondents, while respondents within the “diversity” category represent 48%.

The main difference between both groups is years of experience. The majority group had an average of 21 years of experience relevant to their position, while the minority group had 11. This is particularly important to keep in mind when trying to understand the motivations of respondents to move. Knowing that in both groups, those who have moved from one country to another for their career have done so, on average, in the first five years of their careers, it can be said that early career motivation is drastically different in both groups while motivation further on becomes similar.

Early in their careers, when researchers first moved from country to country, members of the “diversity” group were 30% more likely to move for work-life balance reasons, 25% more likely to do so with the hope of getting higher compensation and 13% for family consideration. On the other hand, members of the “white males” group were 15% more likely to move to change their environments and 10% more likely to do so for skill development reasons. The only reason for a similar score is career advancement in which both score above 4.5 out of 5.

Looking to the future, the highest differences are about work-life balance, family consideration and prestige/recognition in which respondents in the minority group had a 5 or 6% higher score. On the other hand, the majority group is 5% more likely to move for higher compensation. This similarity points towards a cultural space in which members of the minority group have a harder time starting their careers while trying to balance work and the rest of their lives, while their white male colleagues have more headspace to concentrate on personal advancement. More encouragingly, it also points towards a cultural space in which the distinction between groups tends towards a common ground.

Finally, when trying to understand differences in career satisfaction, respondents in the diversity group fall a full point out of 10 lower than their colleagues. This trend can be further extrapolated if subdividing the group into “people of color” and “white women”. In this comparison, white women had better career satisfaction (only half a point behind their white male colleagues) while respondents who identified as a visible minority fared worse, reporting job satisfaction a full two points behind their majority colleagues.

Career stages and stages of life

The survey data divided by years of work experience held by respondents yields some interesting observations. When splitting respondents based on three categories of years of experience, 0-9 years, 10-19 years, and 20+, some trends can be identified. To give some perspective, the first group has an average of 2.8 years of experience, the second an average of 14, and the last 28. It is also noted that only 20% of the first group do not identify as visible minorities, and only 20% do for both other groups; meaning that conclusion coming from the diversity analysis should be considered when understanding the trends highlighted.

From these groups some perspective can be gained on the evolution of motivation through respondents' careers as, on average, the first group moved in the last 2 years, the second group moved on average 10 years ago and the third 22 years ago.

Looking at past motivators to move, it is seen that prestige/recognition, family consideration and higher compensation tend to rise in importance as the years pass; compared to skills development which loses in importance as the years pass. Notable, too, is that change in environment, personal growth and career advancement are of high importance to the least experienced group, then become less important for the middle group and then return to a similar level of importance for the most experienced group, while the inverse trend can be observed for work life balance considerations.

When asked what would motivate researchers for future moves, work life balance is the only motivator that trends from relatively important toward relatively unimportant, while family consideration and prestige/recognition follow the pattern of being more important to those in the middle. All other motivators follow the trend of being of greater importance to either the younger or older group than those in the 10-19-years group.

Still thinking of the future, on average, the younger groups tend to see career advancement, higher compensation and personal growth as the more important motivators when compared to prestige/recognition, family consideration and change in environment. For the middle group, family consideration, career advancement, higher compensation and networking opportunities are the most motivating factors, while work life balance, personal growth and prestige/recognition are less so. For the last group, career advancement, higher compensation and family consideration come out in front, while prestige/recognition, networking/industry opportunities and work life balance fall behind.

For all three groups, career satisfaction is the best predictor of how likely they are to move in the coming years with the youngest group and most respondents scoring higher than average on likelihood to move. The second group, with a satisfaction score of 8.4 and a likelihood to move score of 2.4 skews strongly below the average, with only a handful feeling that they might move. Finally, the group with the most experience has a slightly better satisfaction score at 8.5 and is least likely to move with a 1.5 score with only two in the group scoring high on the motivation to move.

Social Media Self-Representation

Methodology & Caveats

Social Media

Manually scraping data from social media has helped to shine a spotlight on the number of individuals worldwide who identify themselves as part of the international quantum technology ecosystem, but such data comes with the caveat that social media is by no means used uniformly across countries, cultures, genders, and groups. Furthermore, cultural norms and practices may impact the way in which employment status and information are conveyed on social media. For example, China, South Korea and Japan have a very low subscription rates for the social media websites used to gather this data and have cultural norms that may preclude public job searching or broadcasting of career progress. This means the picture drawn from data from social media is a glimpse of the terrain, rather than a detailed map.

One of the challenges of searching for individuals working in quantum jobs and companies is that the word quantum appears in many places that are completely unrelated to quantum technologies. A cursory search of companies listed on standard online website for job seekers yields a dentist office, a law firm, a financial analyst company, a coffee shop, an insurer and a construction firm all with the word Quantum in their company name in the first 13 jobs listed, with only three companies looking for employees with knowledge of quantum technologies.

Data & Analysis

It is not yet possible to give a reliable view of the number of people working in the international and national quantum sectors. The observations that can usefully be drawn from social media data come from comparisons between countries and between different types of quantum business sector (computing, communications, post-quantum security, sensors) and growth trends year-on-year. Despite a strong desire from the QAI team to cite actual numbers of people in the quantum workforce in the world and in individual countries, the data available is simply not reliable enough to allow for this.

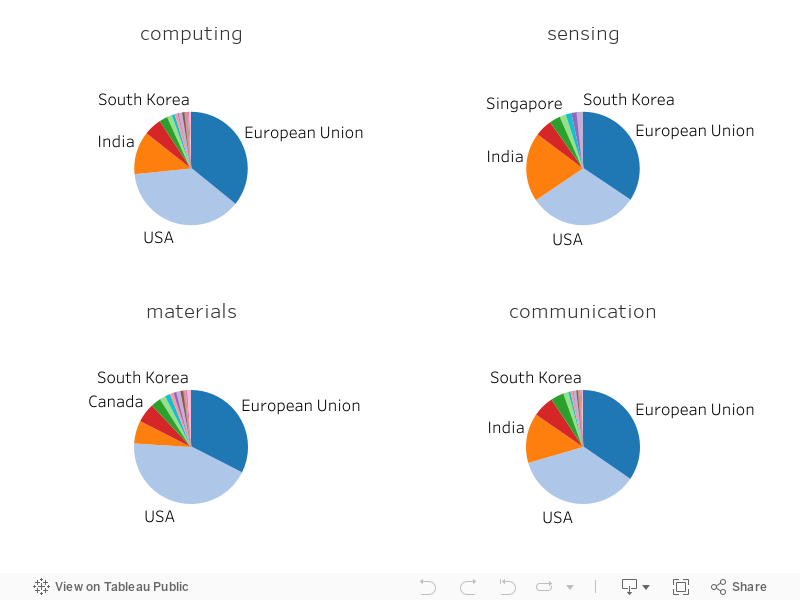

Figure 14. The Global Quantum Talent Pool by Country and by Type of Quantum Technology

Based on social media findings the United States and the European Union dominate the quantum world, hosting around 35% of the world’s talent pool. It is notable that the United States has a significantly larger group of people in materials (44%), and smaller in sensing (31%). This overall lead in the size of talent pools reflects the overall lead that these ecosystems have in the absolute number of people they have in the quantum industry, both in research and in business. Following on is India, which hovers around 15%, but with the inverse of the United States with 7% of people in materials and 20% in sensing. The size of India's overall ecosystem is commensurate with the investment made in the National Quantum Mission, which has seen an investment of US$ 730M from the Indian government.

Canada and Australia hover around 5% and 3% of the talent pool respectively. Both countries show signs of vibrant quantum ecosystems with players in the arenas of both academia and business as they maintain competitive positions overall. While neither country approaches the size of the United States or the European Union, comparison of talent pool size per capita or per GDP shows that both countries are better than average. But the champion of per capita or per GDP weight is Singapore, which hovers around 1.5% of the global quantum talent pool despite its diminutive size.

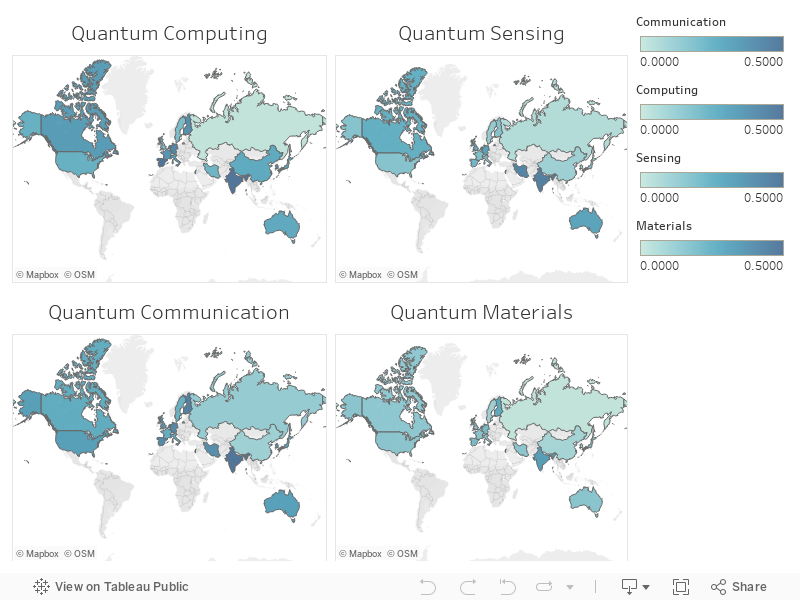

Figure 15. Growth in Quantum Talent by Country and Technology Type, 2023

Compared to 2023, 2024 saw an average growth of around 20% in quantum talent around the world. For the overall quantum industry, Spain is the clear winner with a 306% growth in the last year. This growth has brought them up to speed with other countries in Europe (e.g., Italy and Netherlands). Due to the limitations of the methodology used, the intensity of the growth should be taken as a strong indicator, but cannot be used to form detailed conclusions.

Within Europe, every country surveyed saw growth, with quantum computing and quantum communication seeing the best results. Outside Spain, the countries seeing the most growth are those with larger economies and a strong research ecosystem behind them. This means that the international leads of countries such as Germany and the United Kingdom have only increased. It is interesting to note that Finland has found a solid recipe to grow an ecosystem that is disproportionate to its country size.

In south and east Asia, India has been growing at a faster rate than most, at 30% overall. Should the country sustain that level of growth, India would find itself on the same footing as the United States and Europe within the next decade.

Closer to home, Canada has seen growth comparable to Europe and on average better than the United States, which has somewhat underperformed in terms of growth.

A word about China

While data shows that in 2023, China saw 2% growth across the quantum sector, and with only one subsector, quantum computing, seeing major growth (27%), this finding must be treated with caution. China’s funding, publication, collaboration, and social media practices make it substantially different from any other country included in this study. Researchers included China because China is a major player in the international innovation, industry, and quantum sciences landscape, however, conclusions drawn from the data must be treated with caution, and the Chinese quantum technology landscape is, like the quantum technology landscape, changing rapidly, and growing.

Quantum Skills Requirements

Methodology and Caveats

In September 2023, QAI set out to understand the skills and professional development needs of Canada’s commercial quantum sector. The conclusions of this work were intended to inform the development of upskilling and training programs and support the growth of Canada's quantum workforce.

South Arm Training, a Canadian professional development and education organization, found that the standard databases of information that normally inform their research about employment and skills in any sector – the NOC (jobs), NAICS (industries) and CIP (post-secondary courses) databases – simply did not provide any information about quantum companies, jobs or university programs.

Because of this dearth of standard data, researchers instead collected nearly 60 online job postings from Canadian companies, selecting those with the word ‘quantum’ in the job description, and weeding out any that were not related to quantum physics and associated technologies (for example, ‘quantum health products’, shelving, or portable speaker systems) to provide a starting point to understand the skills requirements of Canada's quantum sector.

Data and Analysis

Overview

All but two of the 60 job postings reviewed were at quantum companies. The other two were at a single company that is a customer for quantum solutions - a company known to be using quantum computing to solve logistics challenges.

Almost all the jobs were technical – focused on hardware engineering, software development and engineering, and research (researchers, lab technicians, etc.). This is not surprising as most of Canada's quantum companies are focused on building their technologies and products. It was noted that job postings outside Canada at larger, established players in quantum computing (e.g., IBM) were heavily focused on business development and sales roles. It is expected that, once B.C. companies are fully in the marketplace, a similar shift in recruitment will happen.

Education and experience requirements

Almost all postings required post-secondary education in a STEM discipline (physics, engineering, etc.) with a preference for graduate (masters/PhD) degrees, although most postings were quite broad in their descriptions. It was clear that the industry is accepting people with a STEM background who are interested in moving into quantum computing from adjacent fields.

More senior roles in engineering had requirements for direct experience in the quantum industry or research, but many also were looking for 5+ years of experience in traditional hardware or software engineering and an interest in quantum technologies. Generally, the more senior the role, the more the job postings were focused on a specific type of engineering/technology, while junior roles required less (between 1-5 years) experience, and not necessarily in the quantum sector.

Technical skills

The range of technical skills required varied due to the specific technologies that companies are developing, but broad experience in related fields (hardware engineering, software development, database management, mechanical/electrical engineering, etc.) were highlighted.

Over half of the postings requested familiarity with programming in Python and to a lesser extent C++ and other programming languages as desirable experience.

Transversal Skills

Communication and collaboration skills figured prominently in almost all the postings, with many references to “fast paced”, “startup”, or “R&D” environments. The ability to work with cross-functional or multidisciplinary teams, attention to detail, motivation, and ability to work to tight timelines and schedules were also highly represented, as were critical thinking and problem-solving.

Quantum Skills Requirements

Most job postings in Canada's quantum computing industry were at quantum computing companies, with a focus on technical roles in hardware engineering, software development, and research. Experience in related fields, such as traditional hardware or software engineering, was commonly required, particularly for senior positions. Many companies also expressed a preference for candidates with post-secondary education in STEM disciplines, including graduate degrees. Proficiency in programming languages like Python and C++ was highly desired.

In addition to technical skills, employers in the quantum computing industry highly value communication, collaboration, and adaptability. Successful candidates would be expected to work in fast-paced, start-up environments, or with R&D teams, requiring effective collaboration across multidisciplinary groups and attention to detail. Critical thinking and problem-solving abilities are essential, as well as the ability to meet deadlines and work efficiently in dynamic environments.

This cameo of skills requirements for Canada's quantum sector provides a useful starting point and QAI researchers are working to gain more and more accurate information to characterize the skills requirements for Canada's quantum companies and for companies that will purchase and use quantum solutions.

Conclusion

The quantum sector is changing rapidly. Companies, investments, national strategies and sovereign technologies are all areas of focus as countries continue to fund growth. Despite financial tightening, private equity investments in quantum startups still reached $1.71 billion in 2023. The second largest private investment globally - US$100 million - was made in Canadian start-up Photonic Inc.

Advances in science and engineering are being made in companies around the world, bringing the prospect of a scalable, fault tolerant quantum computer closer - moving from a 20-year science project to a 5-year engineering project.

Accurate data on Canada’s quantum labour market remains scarce due to the sector's infancy and the lack of national data collection benchmarks. QAI estimates that Canada's commercial and academic quantum talent pool stands at 4,000 people - just 0.01% of Canada's 40 million population. Internationally, workforce data is similarly elusive, although available information suggests that the global talent pool for quantum is proportionately similar to or smaller than that in Canada.

Canada is punching above its weight in all aspects of quantum. Analysis of social media reporting shows that Canada is home to 5% of the world's quantum talent pool, although Canada represents only 0.5% of the world's population. Canadian researchers ranked 10th most prolific in the world, authoring 1,000 of the 75,000 quantum computing research papers published on arXiv in 2023. Canada has a vibrant quantum business sector with quantum computing and software companies such as D-Wave, Xanadu, Anyon, Photonic, 1QBit and Good Chemistry leading internationally on commercialization, scientific advances and development of market-ready quantum solutions.

Despite the paucity of traditional industry data, QAI is working to build a more accurate picture of Canada’s quantum ecosystem and its status in the world. Early insights suggest that there is still a net brain drain (mainly from Canada to the US) that salaries in quantum companies in the late 2010's were on the low side for the tech sector and that women represent 20% of Canada's quantum talent pool and were being paid less than men in the sector in the period from 2017 to 2021. It is also clear that millennials (born between 1981 and 1996) are a driving force in Canada's quantum talent pool.

The flurry of patent filings in Canada since 2015 points to quantum technologies transitioning out of research labs and into companies reflecting the increasing pace of international competition to deliver scalable, fault tolerant quantum computing. Canada's 47-plus domestic quantum companies are closely linked to Canadian universities and are mostly small Canadian controlled private companies (CCPC). Canadians also own 14% of all quantum-technology-related patents filed in Canada. Research patents lag commercial patents, but research continues to deliver important and innovative findings.

The quantum computing market is projected to reach US$45 - $131 billion by 2040. However, the paucity of quantum talent - in Canada and around the world - threatens to slow progress towards this high-value market opportunity. With talent shortages in established high tech sectors and international competition for highly qualified personnel (HQP) in Artificial Intelligence and other deep tech fields, the nascent quantum sector will require innovation in education, training and workforce development to reach its full potential.

Post-Script

This is QAI's second report analysing the Canadian Quantum Ecosystem. QAI researchers have been able to refine some of the data collected to improve the accuracy of reporting, but the sector is still too young to have the benefit of reliable national or international data to provide a sound understanding of the quantum workforce and the skills needed to grow the sector.

Additional data from Canada's federal government, from Quantum Industry Canada and from professional development and education specialists, South Arm Training, working with QAI have provided useful insights. QAI is grateful for access to this information and will be collaborating with these and other partners to improve the quality of information available in the 2025 version of this report.

Data Analyst & Authors

-

Louise Turner

CEO, Quantum Algorithms Institute

-

Yoan Mantha

Data Analyst, Quantum Algorithms Institute

Footnotes

- Quantum Technology Monitor, McKinsey Digital, April 2024, page 11

- Quantum Technology Monitor, McKinsey Digital, April 2024, page 18

- Quantum Technology Monitor, McKinsey Digital, April 2024, page 28

- National Occupations Classification system

- Government of Canada. North American Industry Classification System (NAICS) Canada 2022.

- Statistics Canada Classification of Instructional Programs (CIP) Canada 2016.

- Quantum Technology Monitor, McKinsey Digital, April 2024, page 25

- Business Wire Press Release, 29 April 2024

- Australian Geographic. Australia just invested in a near-$1b quantum computer, what makes it so special, and is it worth the cost? Christopher Ferrie, 6 May 2014

- Quantum Technology Monitor, McKinsey Digital, April 2024, page 28

- The Global Semiconductor Talent Shortage: More than 1 million additional skilled jobs by 2030. Deloitte. 2024 market size and workforce estimated by QAI.

- Lessons from the AT&T Breakup 30 Years Later. Bret Swanson, American Enterprise Institute, 3 January 2104.

- QuEra press release, 6 December 2023

- QuEra Press Release, 17 November 2021

- PsiQuantum Raises $450 million to build Its Quantum Computer, Sara Castellanos, The Wall Street Journal, 27 July 2021